Why Financial Brands Should Put Conversational CX at the Heart of Their Customer Engagement Strategy

December 22, 2021

Modern banking is a very different beast to what was the norm 15-20 years ago. Since the mid 1990s the total number of brick and mortar branches in the UK has fallen by 28% and it’s a similar story in the US, with 12,000 closing between 2010 – 2019. A shift towards using digital services has seen less need for the ‘high street branch’ and has changed customer expectations across the world, part of a wider change in consumer habits that has been accelerated over the past 15 months.

50% of consumers have increased their use of digital banking facilities during the pandemic, with a reported rise of 200% of some banking apps. It’s a trend we’re likely to see stay, with 87% of consumers expecting to continue using digital banking tools once we return to normal – whenever and whatever that may be.

It’s estimated that after only three months of Covid-19 restrictions, there had been a 15% increase in digital adoption, something that might normally happen in the space of 2-3 years. This brings an increased scrutiny on mobile banking apps, where there’s a level of frustration around functionality. Among the biggest complaints are long waits for customer support, unsatisfactory resolution and poor or inconsistent notifications.

The apps covered in the survey were almost entirely traditional institutions, not every bank starts on equal footing when it comes to digital CX. While traditional banks are using digital channels to interact with customers, they are limited in scope with seemingly frustrating native app experiences.

Fintech companies are the fastest growing banks in the UK – with Monzo and Starling seeing a net gain of 43% in new customers in 2020. There’s still some way to go before catching the traditional high street banks in terms of customers, Monzo has 4.8m while Starling broke 2m last year, but they still lag behind giants such as Lloyds with their 17.4m customers. However, they also rank highest when it comes to customer satisfaction among UK banks – citing customer service, application experience, and communication as the standout features.

| Brand | Customer Satisfaction Score |

| Starling Bank | 88% |

| Monzo | 82% |

| Revolut | 77% |

| Halifax | 70% |

| HSBC | 65% |

Source: Which?

There seems to be a shift happening among younger customers which could see the balance tip in favor of financial institutions offering a more user-friendly way of operating. More than 50% of people under 38 see the advantage of challenger banks over traditional providers, citing ease of use and speed of being able to open an account as some of the reasons for it.

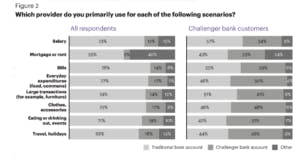

There also appears to be a shift in customers being committed to a single institution for all of their banking needs – instead using traditional and challenger accounts in tandem for different purposes. One thing that the ‘old-guard’ seems to win on is trust, with modern app-based bank customers preferring to use their traditional bank accounts for important financial transactions such as salary, mortgage or rent and bills.

There’s also the perception around data protection that hinders modern brands, who sell themselves as ‘digital leaders’ and offer the promise of getting more out of their data. Only 10% of consumers trust them to protect their data vs 41% for traditional banks.

However, this perception of legacy banking institutions as trustworthy may not be as concrete as they would hope. An American Banker report found public perceptions of top banks are slipping, with the majority of these financial institutions having ‘average’ or ‘weak’ reputations, often weighed down by legacy infrastructure and technology to move with the agility a modern consumer demands.

In fact the majority of Gen Z (62%), Millennials (80%) and Gen X (58%) customers are happy to consider using non-traditional players like Amazon, Apple, Google or Facebook for their financial affairs, with convenience, innovation and better integration into their daily life among the most popular reasons for doing so.

What are Modern Banking Customers Looking for?

Banking doesn’t stand alone in the world of customer engagement. Modern bank customers are also eCommerce or telecoms customers and want similar things from their service providers no matter what the industry, which may be reflected in their willingness to consider tech giants if they offered banking services.

Ease and Simplicity

The days of doing most of your banking in-branch are, thankfully, gone. The average customer has 17 interactions per month with their bank, most of which are online or on their mobile device and, in the US, in-branch transactions have fallen by 40%. These figures aren’t borne out of the pandemic, but BAI found that 84% of people are planning to maintain the same levels of using digital services even when in-person banking resumes, 43% of whom have been doing everything online since Covid-19 hit.

If we consider the appetite for companies like Monzo and Starling in the UK or Chime in the US, and the fact that Millennials, Gen X and Gen Z are all willing to consider tech giants for their financial needs, ease and simplicity are clearly becoming some of the most important factors in banking and financial products.

Personalization

With the desire for ease and simplicity, comes an expectation to not just be lumped in with every other customer when it comes to services and products. Accenture’s ‘Accelerating Digital Transformation in Banking’ report describes this as ‘the Neo Reality’ and is responsible for changing customer expectations.

With companies like Uber and Airbnb setting expectations for what modern experiences of taxis or holidays can be, customers want to dictate how and when they interact with financial service providers. The report found around 50% of consumers expect tailored propositions that address their core financial needs, on top of traditional banking. 40% of consumers are more than happy to switch their banking provider for a more personalized service.

“Technology advances have given businesses access to exponentially more data about what users do and want. It is an amazing opportunity for whoever can use analytics to unlock the information inside, to give clients what they really want.”

PWC

Education and Guidance

While simplicity and personalization are expectations from most consumers of modern brands, the need for education and guidance isn’t something many industries need to deal with. Coming out of a period where money worries have been worse than usual, having access to expert advice on how to ensure financial security will be high on so many consumers’ lists of needs.

It would also appear that having guidance from a human being isn’t a deal-breaker either – 79% of North Americans are open to receiving computer-generated advice on investments, and nearly the same amount would be happy with a bot advising on which type of account to open.

So, with customer attitudes towards what they want from their financial institutions changing, the question is whether traditional banks can rely on legacy market share and historical trust to retain customers if they are lagging behind more modern financial service providers on the experiences that customers are looking for.

Digital Banking is Becoming a Preference After Being a Necessity

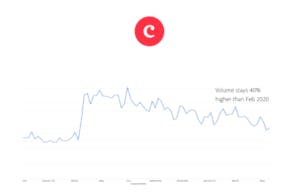

As Covid hit, uncertainty spread through communities across the world. Jobs were at risk, or lost in many cases, which in turn created worries about mortgages, rent, loans or credit card repayments. Millions of people needed to speak to their banks, so it’s no surprise that our data produced the graph below – as you can see, there was an exponential spike in March 2020 across all of the banking institutions we work with.

When we looked closer at one of our traditional banking brand partners, the platform showed spikes in customers wanting to discuss mortgages and loans and getting in touch over messaging channels because they were struggling to get through on the phone. In situations like this, when contact centers are overwhelmed, systems like telephony and webchat struggle to cope with such an unexpected rise in volume. Customers were using messaging channels because it was the most robust method of communication.

The data also tells us that rather than being an anomaly in the early days of Covid-19, messaging volume has remained high. 40% higher than in February 2020 to be exact. For many there’s a bit more certainty in the world, branches are reopening, but messaging channels are still a preferred channel of contact. If the spike was purely down to lockdown, then the number of conversations would have fallen as swiftly as it rose. The convenience, personalization and relationship-centric approach that private messaging channels offer has made them a preference rather than a necessity.

How Financial Institutions can use Private Messaging to Build Long-Lasting Customer Relationships

The rise of modern banking solutions hasn’t brought about a revolution in how people manage their finances, but, alongside Covid-19, the new kids on the block (not those ones) have accelerated consumers’ desire for better digital solutions. Private messaging channels aren’t in a position to replace native apps, but they can be employed to provide exceptional experiences to support the day-to-day activities of mobile banking and satisfy the needs of modern customers.

For Ease and Simplicity

A single place for communication: rather than spending hours on the phone on hold to the bank, then getting frustrated and sending an email while sitting in the queue for live chat, running all customer communications through Facebook Messenger or WhatsApp Business puts the customer in control. Interactions are happening at their convenience, rather than being tied to the phone or website, and agents have access to the entire history of their conversations, meaning they can find context for every interaction, meaning all conversations happen, and can be resolved without having to switch channels.

Opening an account: Verint’s survey of customer habits during the pandemic found that 73% of people looking to open a new account explored digital avenues first. The strength of private messaging channels is they’re designed for both automation and handling volume at scale. Designing a service bot with a specific task can make the process a seamless experience. With a phone and form of photo ID, an account can be opened. The Verint Agent Workspace platform plugs into your system’s APIs and operates on end-to-end encrypted channels like WhatsApp and Apple Messages for Business, so details are safe and secure. The process saves money by automating a task that would often be handled by the contact center and creates exceptional CX for a new customer.

For Personalization

Bespoke alerts: Our State of CX Trends 2021 report found that 81% of people expect brands to offer customer engagement over private messaging channels, and the key to making every notification feel relevant is offering customers the chance to make their own choices. Give them the chance to pick balance or transaction updates or even potential fraud on their accounts, then with tools like Conversocial’s Notify can do the rest by automating the updates and keeping consumers across their financial situation using their preferred channel of communication.

Information on a new product or service: Accenture found that 50% of banking customers want tailored propositions to address their core needs, on top of traditional financial services. With consumers also preferring digital channels, there are really two options for delivering these tailored propositions – contact center agents or intelligent automation. 71% of contact center staff require additional training to discuss new digital products, on top of the costs associated with handling higher volumes. It’s a far better solution for all sides to create automated flows that can guide customers through the decision-making process on the right product for them. It doesn’t need to be every single product, brands can start with one or two, their most regularly requested and build flows around them to start with and iterate from there.

For Education and Guidance

Support across the customer journey: This would very much depend on what a brand’s highest intents are. There can be common questions such as the nearest ATM, with channels like Apple Business Chat or Google Business Messaging, their map functions can be integrated within the chat to show exactly where they are and offer instant directions. For more complex queries, incorporating FAQ responses into service bot flows about products or services can often handle questions that no longer need to be escalated to a human agent, but with the option to do so if it’s a more complex matter. All this creates a far more user-friendly, modern experience for the customer, whilst streamlining a bank’s services.

Banking and financial services are undergoing a shift in operations due to the change in consumer habits, accelerated by Covid restrictions. Rather than seeing ‘challenger’ banks oust legacy brands, we are likely to see both sides start to reflect the best features of the other. Monzo and Starling offer very user-friendly experiences but lack the trust of more established brands, for whom the opposite is true. Legacy systems and bureaucracy can often be blockers to meeting the needs of modern consumers.

By introducing private messaging apps into your CX, as well as being able to interact with customers on their preferred channels, newer brands can build trust through relevant and personalized conversations, while the old guard can provide more digital services in line with the needs of their customers.